Get 5 Investing Tips From a Des Moines-based Financial Advisory Firm

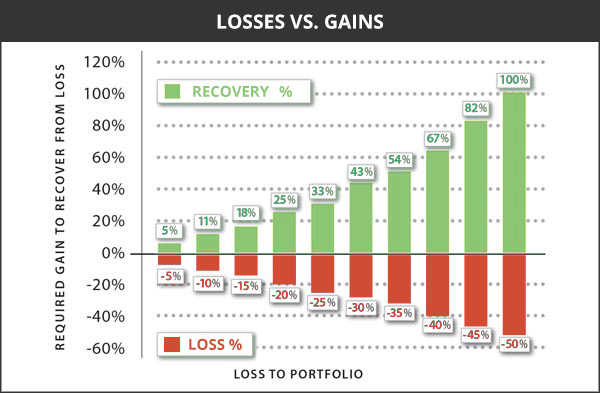

1. Losses Hurt more than Gains Help

All investors are working with one main goal in mind: return on their investment. Every investor dreams of finding the holy grail of investments, a no-risk, high return investment. But as every investor also knows, there is no reward without risk! So, the question becomes if there is no holy grail, what is the next best thing? What types of return end up leading to solid investment growth over time? Is it frequent large gains with only an occasional big loss? Is it smaller, flat, steady returns? Or is it somewhere in between? Most investors do not consider the math behind these questions. In addition, many do not consider how the volatility along the way can greatly impact the outcome. As the chart below shows, a relatively moderate loss can require a much larger gain to bring a portfolio back to even.

Considering investment strategies which minimize the downside potential of your portfolio can greatly increase an investors ability to see higher gains over time. One such strategy is a hedged equity approach. With hedged equity approaches, generally some upside potential during bull markets is sacrificed in exchange for some portfolio protection on the downside. Often times investors believe that if they sacrifice the upside of the market, they will always fall short and underperform the equity markets. On the contrary, for investors who have a proper understanding of the math behind the sequence of returns on their investments and what impacts them the most, they will see investments that result in a lower downside risk can result in a higher net return over time.

2. Roth versus Traditional IRA / 401k debate

Since the Taxpayer relief act of 1997, many investors have had the option of a Roth IRA. The Roth IRA and the traditional IRA bear many of the same benefits to an investor, with the main distinction between the two being how they are taxed. Traditional IRA’s are funded using pretax dollars, so the investor owes income tax when making withdraws in retirement. Roth IRA’s are funded with after-tax dollars, which means an investor will not owe any income tax on qualified distributions. These same basic principles of pretax and after-tax dollars apply to the traditional 401k and Roth 401k accounts, that many employers offer.

Deciding whether a Roth IRA or Traditional IRA is more beneficial to an investor depends on which tax bracket an investors income falls into. When considering conversion at or near retirement the potential for a large income tax bill created by converting traditional pretax dollars to after-tax Roth dollars must be weighed carefully. There is no right or wrong answer when considering conversion, each individual investor will have a unique situation which must be considered and a qualified CPA along with a financial advisor should be consulted.

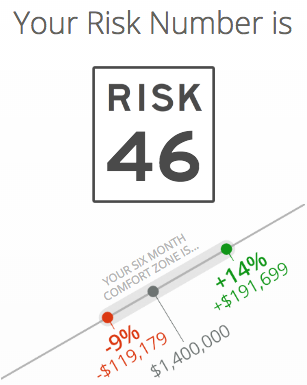

3. Analyzing your portfolio’s risk

We believe investing is broken. Ambiguous terms such as "conservative" or "moderately-aggressive" cause confusion in the investment arena. This uncertainty benefits no one in the advisor-client relationship.

The Risk Number® is an objective, mathematical approach to removing subjectivity by quantifying the risk of investors and portfolios.

The Risk Number is calculated based on downside risk. On a scale from 1 of 99, the greater the potential loss, the greater the Risk Number.

Generalizing client risk tolerance doesn't work. Investors view risk through their own, unique lens to gauge risk and return tradeoffs. The speed limit metaphor helps instill an understanding of that risk. Sometimes it's prudent to slow down depending on weather conditions—the same is true of risk.

Individuals are always evaluating their current location and discerning where they're headed. In the same way, we help investors see what risk they currently have, how much risk they're willing to handle, and how much risk they need to hit their goals. This is the focal point of the Risk Number.

- The road to success begins with understanding how much we possess; that is analyzing our portfolio like using a GPS to know our current location.

- The next leg of the journey is learning our personal Risk Number: being cognizant how fast we're willing to drive. Now we are aware how much risk we have and the risk we can handle. However, there's one thing missing.

- The final stretch is where we map out our short-term and long-term plans to confirm our route and establish the destination.

Once we know these three vectors, we are ready to make actionable decisions about our lives and dreams. Changes may be required, whether taking on less risk because of our risk comfort zone or adopting more risk for a greater likelihood of success.

4. Understanding who you are seeking financial advice from

With many investors concerned about who to trust advice from, it is important to consider the source of the advice. Recent laws designed to protect retirement investors introduced by the Department of Labor (DOL) have also brought the difference between brokers and fiduciaries into the limelight. Many investors are unsure of the difference between a broker and a fiduciary, so here is a great video with a very high level explanation of the differences:

5. Fee’s versus Commissions and where your money goes

Traditionally financial advisors can charge a client in one of a few ways. First an advisor can charge a client an hourly or flat fee to create a financial plan, and or give advice on different financial situations. An advisor can also be a fee-based advisor. This type of advisor will charge a percentage of your assets under management, as their fee for investment and planning advice. The other main type of advisor is a commission based advisor. This advisor will receive commissions from the investment companies which he directs an investors funds too. Commission advisors do not typically charge the investor anything, and the investment company pays the fee normally paid by the client. All three types of advisors have their pros and cons, and an investor should weigh those options before choosing an advisor suitable for them. At First Heartland Financial Group, we have advisors which can use any of the above methods depending on the individual needs and circumstances of the investor.

IF YOU’D LIKE TO LEARN MORE ABOUT YOUR FINANCIAL FUTURE, CALL FIRST HEARTLAND FINANCIAL GROUP AT (515) 273-5120 TO MAKE AN APPOINTMENT TODAY!

Investments are not NCUA insured. Investments are not obligations of or guaranteed by Community Choice Credit Union. Investments may lose value including principal amount invested. Investments and advisory services offered through representative of Lincoln Financial Securities Corporation, member SIPC. Lincoln Financial Securities is not affiliated with Community Choice Credit Union nor with First Heartland Financial Group. First Heartland Group is not affiliated with Community Choice Credit Union. LFS1923484-101617